Preface

The Arctic is warming at twice the rate of the global average. Among many repercussions, scientists have observed a dramatic decline of sea ice over the last few decades. This report seeks to describe to a broader public the current state of Arctic sea ice, explain why this is of great concern to global prosperity, and shed light on the ensuing geopolitical implications.

The Norwegian Climate Foundation and the Nansen Scientific Society share a common goal: to publish, support, and circulate publications that examine climate and its impact on human society. In this joint project we have had the pleasure to engage Sophia Matthews, a Canadian student at Brown University in the United States. Supported by a Nansen Fellowship from the Nansen Scientific Society, Sophia completed this report over the course of an internship at the Norwegian Climate Foundation’s office in Bergen, Norway. This report reflects her findings and opinions on the geopolitical implications of Arctic sea ice melt.

We would like to thank everyone who has contributed to this project, and in particular, Sophia, who has worked hard and purposefully throughout this short internship period.

Bergen, September 3rd 2019

Lars-Henrik Paarup Michelsen

Director,

Norsk klimastiftelse

Ola M. Johannessen

President,

Nansen Scientific Society

Cover photo:

NASA/Kathryn Hansen

The Norwegian Climate Foundation is an independent green think tank. We convey knowledge and ideas to the public about climate change and climate solutions. Our vision is a world without anthropogenic greenhouse gas emissions. The Foundation’s formal network includes Norway’s leading universities, colleges, and research institutions.

Nansen Scientific Society is an idealistic foundation for «Knowledge without borders». Its vision is that education and research within global environment and climate problems, including their impacts on society for students and young scientists from different countries and cultures, will provide a foundation for greater understanding and co-existence in the word – in the spirit of Dr. Fridtjof Nansen.

Acknowledgements

Sophia Matthews

Sophia Matthews (20) is a Canadian student pursuing her Bachelor’s degree at Brown University – an Ivy League research university in Providence, Rhode Island, USA. She studies international relations and environmental science, but her academic interests also include human rights and refugees, environmental economics, and foreign language.

I would like to extend my sincere gratitude to the Norwegian Climate Foundation for affording me the unique opportunity to complete an internship in Bergen; allowing me to research and write about a topic both of personal and global interest. In particular, I would like to recognize Lars-Henrik Paarup Michelsen for his continued encouragement, feedback, and confidence in my own judgement.

I would also like to thank Andreas Østhagen for helping to shape my understanding of Arctic geopolitics, and for pushing me to question the very limits of geopolitics themselves. In addition, I would like to thank the Nansen Scientific Society for the patronage that made my research possible. I owe, in large part, this experience to the sponsorship of the Nansen Scientific Society and the support of Bente E. Johannsessen. Finally, I would like to thank Ola M. Johannessen for his guidance, expertise, and commitment to my work.

Excecutive Summary

The Arctic is warming at twice the rate of the global average. Rising temperatures in the circumpolar region are consistent with greenhouse gas emissions, indicating a causal relationship between anthropogenic forcing and Arctic climate change. Among a host of consequences, Arctic sea ice is declining rapidly, giving way to a changing geopolitical landscape. While the Arctic Eight – Canada, the United States, Russia, Denmark, Norway, Iceland, and Finland – are the primary stakeholders, China has demonstrated significant efforts to legitimize its position as an Arctic actor. Political moves to authority aside, the Arctic is of great concern to the entire planet. As its natural climate systems function to regulate global climate systems and cool the planet, changes to the Arctic climate precipitate global ramifications.

One can expect ice-free Arctic summers by the end of the century. An increasingly cohesive scientific consensus on the prospect of ice-free Arctic waters has inspired research regarding the use of the Northern Sea Route and the Northwest Passage as international shipping routes. Should these Arctic waterways become available for commercial use, transit times could be reduced by up to fifty percent, incentivizing increased bilateral trade between major western European trading ports and northeast Asian states such as China, South Korea, and Japan. However, declarations of a quickly changing international trade picture are ill-founded and overstated. A gaping lack of infrastructure, Russian monopoly on transit fees, high insurance premia, and severe data scarcity are few among the multitude of obstacles to shipping via these Arctic waters. This claim that international trade will soon shift northwards is one among many Arctic myths fabricated by mainstream media, and serves to undermine the true complexity of the Arctic situation.

Popular media also lend to tales of a burgeoning resource war over unclaimed Arctic hydrocarbon riches, implying a causal relationship between melting ice and sovereignty challenges. Again, such claims are exaggerated and uninformed. With ninety percent of Arctic oil and gas accounted for by the jurisdictional limits of Arctic nations, Arctic nations have given no indication of intentions to expand offshore exploration beyond established territorial borders and exclusive economic zones. Discussions of a resource war represent yet another fable; another misconception about Arctic geopolitics.

Retreating ice cover is, however, prompting different reactions from the fossil fuel industries in Arctic nations. Most notably, Russia plans to expand its offshore drilling and exploration, aided by investments by an eager China as relations with the West deteriorate. Other nations such as Canada and Norway, highly dependent on oil and gas exports, toy with sustainable investments in other sectors while their fossil fuel industries run generally unobstructed by calls for climate action. Canada, notably, has instituted a federal moratorium on offshore drilling in the Arctic. The ban was made in partnership with the United States, whose current administration is attempting to repeal the policy.

If one is to retain a single lesson from this report, let it be a word of caution against oversimplification. The Arctic region is climatically and politically complex; it entertains rival narratives of cooperation and competition, hosts eight governments, and harbours hostile and variable climatic conditions. One must remember that the Arctic is a climatic – rather than political – region. Thus it is subject to many diverse political landscapes, its future largely at the mercy of government discretion. To neglect such complexities is to forego a robust understanding of the geopolitical opportunities and challenges that befall the Arctic.

Introduction

The common imagination paints the Arctic as a vast and virgin expanse of snow, dark green coniferous trees iced in thick powder and snow banks caving beneath the tread of the polar bear. This romanticized image of the Arctic neglects the changing geopolitical landscape of the Arctic under anthropogenic climate change, as well as notable nuances and regional differences that demarcate the Arctic. A more technical and scientifically recognized definition of the Arctic denotes the region above the Arctic Circle – a line that circles the globe at 66° 34’N. In these high latitudes, summer temperatures generally do not rise above 10°C. This includes the Arctic Ocean, which incorporates Baffin Bay, Barents Sea, Kara Sea, Beaufort Sea, Chukchi Sea, East Siberian Sea, Greenland Sea, Hudson Bay, Hudson Strait, White Sea, and Laptev Sea. The Arctic also comprises lands and waters belonging to Canada, the United States, Russia, Greenland, Finland, Iceland, Norway, and Sweden. With The Kingdom of Denmark representing Greenland, these eight nations constitute the Arctic Council – an intergovernmental forum that addresses social, economic, and environmental issues in the Arctic.

The Arctic climate is not totally uniform across all its constituent countries. For example, the Canadian Arctic is among the most hostile regions on earth, whereas the Norwegian Arctic is more temperate and habitable. When discussing climate change and the ensuing implications, many refer to “the Arctic” as if the Arctic expanse is so invariable that it can be classified as a single region. This generalization is largely for the sake of simplicity. To avoid losing the big picture to a detailed discussion of the many degrees of variation within the Arctic region, precision is sacrificed for comprehensibility. Thus, although this report will continue to refer to the Arctic in general and unrefined terms, it is important to address the limitations of this approach and direct attention to the true complexities that befall discussions of the Arctic.

Such variation is not limited to climatic conditions – it is also crucial to acknowledge varying geopolitical and economic considerations for Arctic stakeholders. Just as Spain and France share relatively similar climates, but one does not imagine their politics to be necessarily similar, one cannot conflate climatic similarity with geopolitical similarity in the Arctic. Each Arctic actor has unique economic and political concerns. For example, the small American Arctic is far less significant to the United States’ overall economic growth and political identity than the Russian Arctic is to Russia. Or, in sharing a border with Russia, the security dimension of Arctic development is much different for Norway than it is for North American Arctic nations.

All this is to provide a word of caution against sweeping generalizations regarding Arctic climate and geopolitics. One must pay due attention and respect to the intricacies and variations within the Arctic. It is worth considering that we, as a human species, may still be largely uninformed about the degree of variation and the true consequences of such subtle differences within the Arctic; it remains a relatively unfamiliar region.

Climate Variability and Climate Change

Since the onset of the 20th century, the Arctic and its oceans have seen dramatic climatic changes. The years 1910-1940 were met with a widespread warming of the Arctic, followed by a cooling that lasted until 1970. Early 20th century warming was only observed in the Arctic region and was caused by long-term variability inherent to Arctic climate systems, called Atlantic Multidecadal Oscillation (AMO).1 Other inherent features of the Arctic climate include seasonal fluctuation of ice coverage.

Besides this, a host of other factors and phenomena influence sea ice coverage, such as surface air temperature, ocean circulation patterns, cloud cover, water vapour content, and heat fluxes, among others. It should be noted that September marks the end of the normal summer melt season, and the lowest ice coverage in any given region on an annual scale. Conversely, March represents the peak of the cold season and the maximum Arctic ice coverage on an annual scale. This report will frequently reference September and March as benchmark months to compare current and projected trends with observed data.

Source: Arctic ROOS

Climate within the Arctic is also variable. Maritime climates, such as those in northern Russia, Scandinavia, and Iceland, are characterized by stormy and wet winters, balanced by cool and cloudy summers. Contintental Arctic climates are dryer, with more severe winters and more sun exposure during summer.2 This is notable because it illustrates the obstacles and limitations inherent in envisioning the Arctic as uniform and unfluctuating. The general volatility of Arctic climates and weather patterns present a significant obstacle both to projections regarding future climatic conditions and the navigability of Arctic waters.

A distinction must be drawn between internal climate variability and anthropogenic climate change. While a certain degree of variability is innate to the regular functioning of the Arctic climate, today’s observations surpass the normal bounds of internal variability. Moreover, they are consistent with greenhouse gas emissions and evidence of anthropogenic forcing – this era of warming is fundamentally different than the warming observed in the early 20th century.3

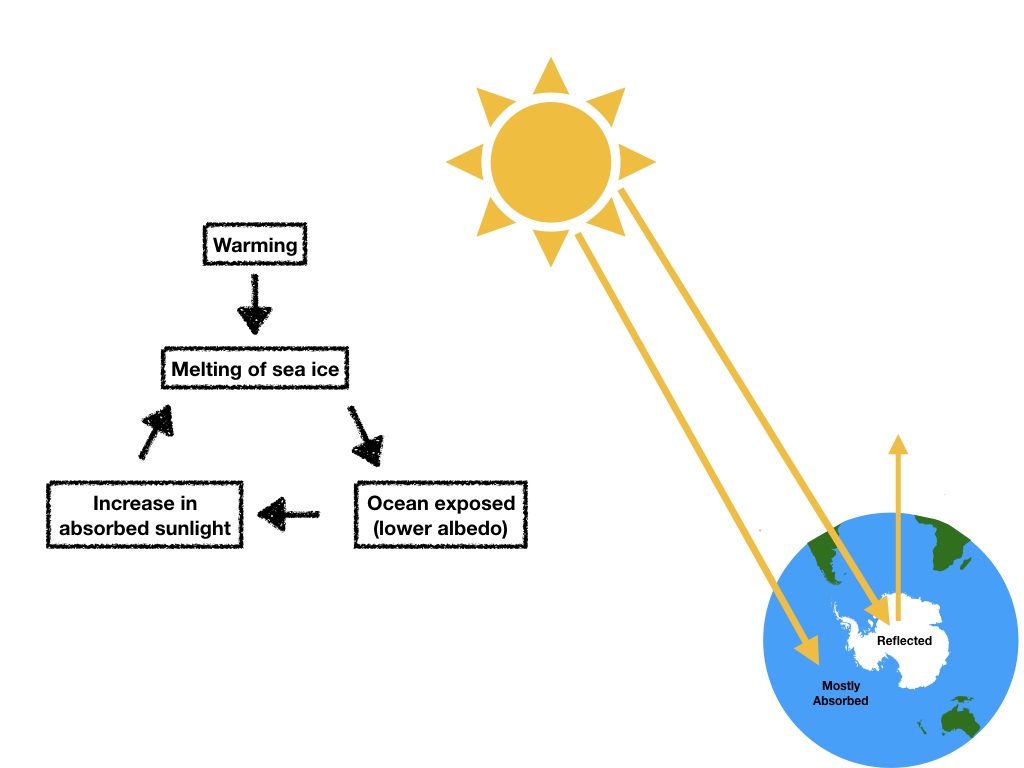

Within the context of anthropogenic climate change, perhaps the most significant feedback to consider is the albedo effect. Albedo is a measure of the reflective capacity of an astronomical body or a given surface. Lighter surfaces, such as snow and ice, have a greater reflective capacity than dark surfaces, such as land and open water, that absorb sunlight and heat. As Arctic sea ice melts and gives way to open water, earth’s albedo decreases. The albedo effect is self-reproducing – as ice melts and albedo decreases, more heat is absorbed, which, in turn, further melts ice.

Arctic Amplification

The Arctic region has warmed more than any other region on Earth over the course of the last thirty years. Surface air temperature in the Arctic has increased at twice the rate of the global average – this has been termed Arctic amplification.4 Arctic amplification is most pronounced during autumn and winter. When air temperatures drop below ocean temperatures in the colder months of the year, heat accumulated in the uppermost layer of the ocean during summertime is transferred to the lowest layers of the earth’s atmosphere. In simple language, Arctic waters lose the heat gained throughout the summer to the atmosphere in colder months.5

There is generally little consensus as to the relative importance of different factors that influence Arctic amplification, and still a significant portion of Arctic amplification remains unexplained. Scientific knowledge of Arctic systems is limited by a mere one hundred years of temperature records and the high variability of climatic conditions on annual and decadal scales. However, the current understanding of Arctic amplification cites albedo – and thus, sea ice decline – as a primary driving mechanism.6 Sea ice plays a pivotal role in the exchange of heat between open water and the atmosphere. As melting ice gives way to open water, heat is accumulated in the upper ocean layer. This translates to larger heat transfers from the upper ocean layer to the troposphere in the colder seasons of the year, thus concentrating warming near the surface in the lowest layer of the atmosphere. One should imagine sea ice and upper layer heat as competitive: sea ice reduces the surge of heat from open water to the atmosphere, while, conversely, the heat accumulated in the upper layer of the ocean delays the build up of ice and reduces its thickness. This thinner ice is more readily melted the following summer, leading to more open water in September and further heat accumulated in the ocean’s upper layer.7

The relationship between Arctic amplification and the albedo effect signals the impact of human activity on the Arctic climate. As human activity generates greenhouse gas emissions, which affect albedo, and albedo is a primary driver of Arctic amplification, anthropogenic forcing is linked to the enhancement of Arctic amplification and thus the warming of Arctic waters and the melting of sea ice.

Source: Wikipedia

The Earth’s Thermostat

The albedo effect is important for understanding why Arctic sea ice loss represents potentially catastrophic global repercussions. It is worth noting that land ice formations such as glaciers and ice sheets are also important considerations for the future stability of the Arctic and global climates. In particular, Antarctic ice formations and the Greenland ice sheet represent looming threats to global sea levels. The melting of such major ice sheets – well underway due to anthropogenic climate change – may endanger major urban centres such as London, Hong Kong, Shanghai, and New York.8 While land ice melt is a pressing issue, this report shall focus on sea ice melt in the Arctic – which does not contribute to sea level rise – and exclude discussions of land ice at both global poles.

The Arctic is a heat sink, meaning it reflects more heat than it absorbs from the sun’s rays, thus functioning to cool the entire planet. Historically, the Arctic as had high albedo relative to the rest of the earth’s surface, due to its high concentrations of snow and ice. As these reflective surfaces disappear, the Arctic’s albedo decreases, catalyzing further ice melt and warming waters. Arctic waters and atmosphere are responsible for generating energy flows from the tropics to the poles. Without this energy transfer, the tropics would overheat to the point of becoming inhabitable. The Arctic Ocean is also a major vessel for energy transfer within the Northern Hemisphere.9 In short, Arctic climate systems serve to regulate climate and weather across the globe. Thus, changes to the Arctic climate are potential changes to the global climate – the consequences of disruptions to Arctic systems are far from confined to the Arctic circle.

Part I: Climate Change & Melting Sea Ice in the Arctic

Arctic Sea Ice in the 20th Century

Since satellite observations began in 1979, there has been a significant decrease in Arctic ice coverage. This comes as a surprise to few – the fabled tale of greenhouse gas emissions and the perils of anthropogenic climate change are, by now, familiar to most. Although models differ as to exact dates of record high or low ice coverage and exact measurements of ice coverage in a given year, these statistical differences are negligible when considered in the context of uniformity across all credible models in terms of calculated trends: Arctic ice coverage is decreasing rapidly and linearly.10

Models estimate that between 1915-1940, when the Arctic underwent warming as a consequence of long-term variability and AMO, between 240,000 and 580,000 km2 of sea ice was lost. Although there are discrepancies between models due to technological limitations as to when ice coverage was highest in the 20th century, most range from early to mid century.11 According to the Intergovernmental Panel on Climate Change (IPCC), average temperatures increased by up to 5°C throughout the course of the 20th century. Additionally, water flows between the Atlantic and Arctic Oceans warmed, and terrestrial permafrost decreased significantly.12 The late twentieth century saw the onset of the steep decline in sea ice coverage that has peaked in more recent years, consistent with anthropogenic forcing and increased greenhouse gas emissions. Although sea ice variability is at the mercy of multiple climatic factors, such as surface air temperature, ocean circulation patterns, and cloud cover, climate models indicate that 90% of Arctic sea ice loss since 1970 can be explained by increases in atmospheric CO₂.13

Source: Nansen Scientific Society, Nansen Environmental and Remote Sensing Centre

Arctic Sea Ice in the 21st Century

Scary Statistics

- Arctic surface air temperature warming has escalated rapidly since 1998, with stronger warming trends and conspicuous sea ice reductions over the Barents, Kara, Chukchi, and East-Siberian Seas.14

- This has been consistent with increasing greenhouse gas emissions.

- Surface air temperatures between 2014-2018 were greater than any year since records began in 1900.15

- The twelve lowest minimum sea ice extents in the satellite record have all occurred in the last twelve years.

- Maximum sea ice extents from 2015-2018 were record lows.16

- The lowest observed value of total September ice coverage occurred in 2012, at 4.2 million km2. This is 3.3 million less than the 1979-2005 average.17

- In other words, 2012 ice coverage was just 56% of the recorded average.

- Between 1979-2017, September ice cover decreased by 10.6% per decade, amounting to a staggering 40% total decrease.

- In the same time period, March ice cover decreased by 10%.18

Multi-year Ice

In addition to total ice cover, the ice age distribution has undergone substantial changes since the 20th century. Multi-year sea ice – ice that has survived at least one summer melt season – is decreasing more rapidly than newer ice, due to the accelerating rate of ice melt and the impact of Arctic amplification on the thickness of ice. In the 1970s, multi-year ice accounted for more than two thirds of the total surface area of the Arctic basin. By 1985, multi-year ice accounted for only half of total ice coverage. Since, average multi-year ice cover has decreased by roughly 17% per decade, or about 846,000 km2 in a single winter season.19 By 2015, the ratio of first-year relative to multi-year ice was essentially flipped from the 1970 precedent: multi-year ice accounted for less than one third of the total surface area. In 1985, twenty percent of March ice cover was four years or older. By 2015, this had decreased to just three percent.20

Projections: Present to 2100

Current projection models often centre on the possibility of an ice-free Arctic or ice-free Arctic summer. Due to the high variability of the Arctic climate and varied projections regarding concentrations of atmospheric greenhouse gases, estimations differ as to when exactly an ice-free Arctic summer might occur. The majority of models predict an ice-free summer around mid-century, whereas some estimate as early as 2030 and more conservative calculations place an ice-free summer between 2066-2080.21 Prior to a massive sea ice collapse that occurred in 2007, the IPCC predicted that an ice-free summer would occur at the tail end of the century. The 2007 collapse served as something of a wakeup call – now, many popular climate models estimate catastrophic sea ice reductions in the 2020s and 2030s, and ice-free conditions by midcentury.22 It should be noted that estimations of an ice-free summer correspond to forecasts of atmospheric greenhouse gas concentrations – models that predict higher concentrations estimate earlier ice-free conditions, and models that predict lower concentrations estimate later ice-free conditions, emphasizing the causal relationship between anthropogenic forcing and Arctic ice melt.23

Source: Science Direct

The Barents Sea

- Currently ice-free from July through October. The ice-free period will gradually expand to June through December.

- Expected to be permanently ice-free before 2046.24

The Kara Sea

- 80% of total sea area has been ice-free since 2000.

- Projected to be ice-free from July through October by 2047, and from June through December by 2074.25

Other Arctic seas

- The difference between the winter maximum and summer minimum ice cover in the East Siberian and Beaufort seas was four times greater in 2016 than it was in the 1980s.

- The same difference was tripled for the Laptev and Chukchi seas.

- 2010-2016 marked the first time over 80% of its total sea area in the Laptev sea was ice-free. This is among the largest fractions of observed ice-free sea area in the historical record.

- By the end of the century, 80% of total cumulative sea area in the Barents, Kara, East Siberian, and Chukchi seas is expected to be ice-free.26

The Arctic climate is impacted by a myriad of environmental issues aside from climate change – chemical contamination, overfishing, and habitat destruction, for example. Although it is important to remember that climate change interacts with this multitude of other environmental issues, greenhouse gas emissions are of cardinal consideration with respect to melting sea ice and the ensuing consequences. To put the gravity of greenhouse gas emissions in perspective: according to the Arctic Council, anthropogenic climate change was responsible for 70% of global glacier loss between 1991-2010.27 If current trends continue, greenhouse gas emissions are projected to contribute to 4-7°C of warming within the next century, in addition to the 2.7°C of warming that occurred between 1971-2017.28

Summary

The accelerating decline in Arctic sea ice is among the most visible and alarming consequences of anthropogenic forcing. The last four decades have seen unprecedented changes to the Arctic climate and landscape – currently observed sea ice trends exceed predictions made by past models.29 These drastic changes are consistent with atmospheric concentrations of greenhouse gases. Although, due to high climatic variability, exact dates are hard to estimate, climate models project that Arctic waters will become seasonally ice free by mid century if emissions continue at current levels. Most notably, the vast majority of sea area in the Barents, Kara, East Siberian, and Chukchi seas is expected to be ice-free year-round before the end of the century.

Repercussions to wildlife, Indigenous and other human communities, and global climate systems aside, melting sea ice in the Arctic Ocean is significant because it opens up previously blocked shipping routes in the Arctic. The Northern Sea Route and the Northwest Passage have recently been given increased attention in discussions of international trade and security.

Part II: Trade & Shipping Routes

The Northern Sea Route

The Northern Sea Route (NSR) is shaped by the Kara, East Siberian, and Chukchi seas. There is no single route that defines the passage – the NSR refers to multiple possible routes that can vary in length between two and three thousand nautical miles.30 The NSR was first opened for foreign use in 1991. The first commercial transit of a non-Russian vessel occurred in 2009, followed by a non-Russian bulk carrier and liquified natural gas (LNG) tanker in 2012.31 2013 saw a 65% increase in the number of NSR voyages from the previous year, but this corresponded to a cargo increase of a mere 7.5%.32 The vast majority of these voyages weren’t fantastical international shipping escapades; over sixty percent of these voyages were between two Russian ports.33 Still, annual voyages are – albeit very slowly – steadily increasing. Between January and April of 2019, forty nine vessels, amounting to 426 voyages, passed through the NSR.34 Of these voyages, roughly 36% were tankers, 28% were LNG carriers, 15% were container ships, and 20% were icebreakers, and 60% of total voyages in 2019 bore the Russian flag.35 The total volume of traffic in the NSR in 2018 amounted to 20.2 million tonnes, and Russian President Vladimir Putin has pledged to increase this figure to 80 million by 2024.36

Source: CPB Netherlands Bureau for Economic Policy Analysis

Sovereignty

The legal status of the NSR has long been a topic of debate, but sea ice decline has drawn increased attention to sovereignty concerns. Given that the NSR runs through internal waters and territorial seas of the Russian Federation, Russia views the NSR as a “historically established national transport communication of the Russian Federation”, and maintains an authoritative regime for the navigation of vessels through the passage.37 Notably, the development of the NSR to date has been exclusively carried out by Russia. Many scholars argue that these historical development efforts and unparalleled – although limited – experience and knowledge of the area strengthen the Russian claim to jurisdiction.38

Russian authority, in practice, has been challenged. In the first ten months of 2017 alone, almost one hundred violations of the NSR Rules of Navigation were recorded by the Russian Northern Sea Route Administration (NSRA). This represents almost twenty percent of all ships to pass through the NSR that year.39 The greatest challenge to the Russian claim stems from differing interpretations of the 1982 United Nations Convention on the Law of the Sea (UNCLOS). The United States has accused Russia of interpreting its provisions too broadly in order to introduce discriminatory measures and restrict navigation, and frequently harkens back to the provision of the right to “innocent passage”.40 In particular, UNCLOS provides certain privileges under and restrictions for “ice-covered areas” – thus, as the Arctic physical landscape changes, as does the interpretation and implementation of international law. The US has adopted perhaps the most radical view among Arctic nations that all Arctic straits are international waters and no single state can restrict passage of international vessels.

In rebuttal, Russian officials claim that the legal regime of the Arctic as a whole – and thus, the NSR – derives not only from contractual and customary law, but also the domestic law of Arctic nations.41 The Russian Federation seems perpetually met with a dilemma of balancing a defence of its sovereignty with the economic benefits of liberalizing the NSR. The Russian government has actively underlined its intention to develop and modernize the NSR for international shipping purposes. At the 2011 International Arctic Forum, while simultaneously emphasizing Russia’s jurisdictional authority, President Vladimir Putin is quoted: “We are planning to turn it into a key commercial route of global importance. I’d like to emphasise that we see its future as an international transport artery capable of competing with traditional sea routes in cost of services, safety and quality”.42

Bilateral trade: Northeast Asia and Northwest Europe

Currently, eight percent of global trade passes through the Suez Canal, which allows ships travelling between the global East and global West to avoid the long detour around the Cape of Good Hope.43 With ice-free conditions projected for Arctic seas by mid-century, the possibility of redirecting trade through Arctic waters has become a popular topic of discussion in commercial and political contexts. Connecting Northeast Asia with Northwestern Europe, it is estimated that two thirds of trade currently passing through the Suez Canal could be rerouted through the NSR. Travel via the Suez Canal from east Asia to Europe is roughly 21,000km. Using the NSR, this could be reduced to 12,000km, which would cut travel time by ten to fifteen days.44

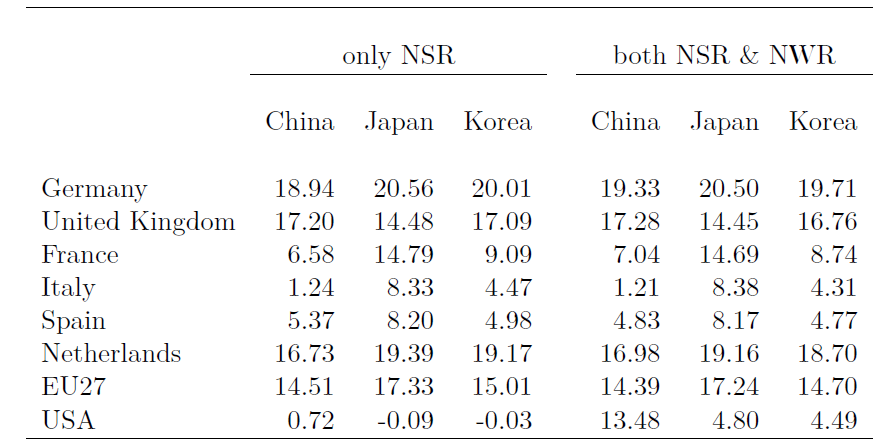

Analysts forecast that an ice-free and operable NSR would increase total global trade. This increase would be concentrated in Northeast Asia, with China, Japan, and South Korea increasing trade with western Europe by roughly ten percent.45 By redirecting trade through the NSR rather than the Suez Canal, the distance from Japan to major European shipping ports in the Netherlands, United Kingdom, Germany, and Belgium would be reduced by 37%. The distance from South Korea and China to the same ports would be reduced by 31% and 23% respectively.46 In some cases, transit distance could be cut in half. For example, the distance from Yokohama to Rotterdam via the Suez Canal is 20,000km. Should the NSR become fully operable, the distance between these two ports could be reduced to less than 9,000km.47

Source: CPB Netherlands Bureau for Economic Policy Analysis

However, reductions in shipping distances do not necessarily correlate to reductions in cost. Cost savings must be weighed against increases in trade volume – western European and east Asian economies are likely to take advantage of an operable NSR and increase bilateral trade flows amongst themselves. Thus the total cost savings generated by an open NSR are difficult to predict, as a host of external factors may influence the degree to which each nation chooses to increase trade flows. Based on the capitalist dogmas that govern modern economies, it can be reasonably assumed that many nations, granted financial leeway by reduced transit distances, would increase trade flows – particularly since Asia has overtaken North America as the largest market for European exports.48 Analysts predict that, under fully operable conditions, Germany will increase trade with Northeast Asia by 11%, and that a similar pattern would be replicated by Austria, Belgium, Denmark, Finland, France, Germany, Ireland, the Netherlands, Sweden, and the UK.49

Simulations of full NSR operability show that this would result in trade diversion – bilateral flows between western Europe and China, Japan, and South Korea will increase at the expense of trade with other regions. In particular, intra-European trade will decrease, namely between Northwestern Europe and the southern and eastern parts of the continent.50 This trade diversion must be weighed against trade increases with Asia. Some countries, such as France, Spain, and Portugal, are expected to increase trade with Asia by only 1-3%. Since this would not compensate for the reduction in intra-European trade, the opening of the NSR would not change the overall trade picture for these countries.

Practical feasibility

Predictions of increased trade flows are tempting, for northwest Europe and northeast Asia in particular. However, it is important to address the limitations and shortcomings of these predictions. There are many obstacles that must be overcome in order for the NSR to become a financially sensible pursuit. Namely, projections for sea ice decline often overlook the complexities of the Arctic environment. First, declining sea-ice does not necessarily guarantee open routes. Take for example 2007: a year whose ice extent was 24% lower than the previous record low, and 37% lower than the 1979-2007 average.51 Although one might have imagined this massive collapse of sea ice as a blessing in disguise for Arctic shipping, the NSR was still blocked.52 Melting ice increases the risk of encountering drifting ice and small icebergs, which are difficult to detect and would force ships to drastically reduce their speed, therefore potentially offsetting time gained from shorter routes.53 In addition to technological limitations in predicting Arctic weather, other environmental factors such as extreme cold, fog, poor visibility, and violent wind pose threats to the practicality and safety of using the NSR.54

Moreover, reduced shipping distances cannot be conflated with reduced costs. Today, commercial vessels can navigate the NSR, but only under very good weather conditions and escorted by icebreakers.55 A study commissioned by the Arctic Council estimates that the NSR will only be navigable without icebreakers for ninety to one hundred days per year by 2080.56 With such a short window of opportunity appearing only towards the end of the century, icebreakers are necessary to make the NSR profitable for shipping companies. Such icebreakers incur an additional cost to those hoping to safely pass through the NSR, in addition to the logistical costs of inspection.57 As per current Russian regulations, only Russisan icebreakers may provide assistance to ships passing through the NSR.58 Thus, shipping companies remain at the mercy of a Russian monopoly on icebreaker fees. Currently, the Russian tariff system charges on the basis of cargo volume only. Although tariffs have been reduced in the last decade, the cost per tonne still ranges between $20 and $30 – a hefty fee compared to the mere $5 per tonne charged for transit via the Suez Canal.59 Although discussions of altering the tariff system are ongoing, until significant changes are made, the fees per tonne of cargo are hardly competitive with conventional use of the Suez Canal.

Icebreakers and transit fees are among many investments necessary to navigate the NSR – the true costs of navigating Arctic waters are frequently understated. For example, hostile weather conditions translate to higher insurance premiums that must be borne by shipping companies. The potential that this may offset money saved, plus the risks and uncertainty associated with Arctic weather is frequently cited as a cause for hesitation by shipping and cargo companies.60 Vessels must also file a permit with the Russian Administration of the NSR four months in advance, while permits to traverse the Suez Canal only require forty eight hours advance notice.61 The customs clearance and fees placed on navigating Russian waters consist other logistical and financial considerations.62 As if the list of financial obstacles isn’t long enough, the standard GPS system is currently unavailable in the NSR. Ships looking to navigate these Arctic waters would have to transition to an alternate system called GLONASS, which is incompatible with some existing ships.63 Furthermore, infrastructure along littoral lands and Arctic waters is severely limited, which implies significant safety and environmental concerns. The NSR has scarce loading and unloading docks, inadequate search and rescue capabilities, and few relief ports.64 This lack of infrastructure exacerbates weather-related concerns, in that the NSR is currently inadequately equipped to handle spills, accidents, unforeseen weather conditions, mechanical damage, or emergencies. Under present conditions, cargo and personnel navigating the NSR would be unlikely to receive necessary assistance in a timely manner. All these complications considered, some analysts calculate that the NSR would only be competitive with the Suez Canal when the price of fuel is low, the NSR is open for a minimum of three months a year, and Russian transit fees are reduced by 85% of their 2010 levels.65

In short, the navigability of the NSR is not simply a question of declining sea ice extent. Even under ideal shipping conditions, there are still several logistical, financial, and infrastructural hurdles to overcome. All this considered, regardless of sea ice conditions, the likelihood of the NSR becoming competitive with the Suez Canal is, at best, questionable.

The Northwest Passage

History

The Northwest Passage (NWP) mirrors the coast of North America and connects the Northern Atlantic to the Pacific Ocean via the Arctic Ocean and waterways in the Canadian Archipelago. The vast majority of vessels in the NWP operate along the southernmost parts where conditions are more favourable; northern parts of the passage are almost exclusively used by government vessels and accompanying icebreakers. Traffic in the NWP almost tripled between 1990 and 2015.66 Cargo ships and government vessels, including icebreakers, account for the largest share of traffic, whereas private yachts and pleasure craft are the fastest growing – in the same time period, tourism transit increased by more than twenty fold. Cargo vessel traffic also saw a steep increase in 2007, when the NWP was ice-free for the first time on satellite record.67 A glaring obstacle to the lucrative potential of the NWP is major data scarcity. Few reputable studies have been made to establish any sort of significant consensus on the future of traffic in the NSR.

Source: International Journal of Trade and Global Markets

Sovereignty

Sovereignty challenges to the NWP have historically represented the greatest threat to Canadian sovereignty. Canada treats the NWP as internal waters subject to Canadian jurisdiction; in 2009, the Canadian House of Commons resolved to rechristen the Northwest Passage the Canadian Northwest Passage.68 Others, and the US in particular, protest this claim and demand that the NWP be legally considered international waters where foreign and military vessels have the right of passage.69 In 1985, a US Coast Guard icebreaker transited the passage from Greenland to Alaska without first seeking the permission of the Canadian government. This inspired the 1988 Agreement on Arctic Cooperation, which “pledges that all navigation by US icebreakers within waters claimed by Canada to be internal will be undertaken with the consent of the Government of Canada”.70 When NATO increased its presence in the Arctic in the early 21st century, this undermined Ottawa’s relative power and presented a threat that the compromise with the US might unravel.71

These challenges to Canadian jurisdiction over its Arctic have resulted in sovereignty anxiety – the perception that Canada is struggling to uphold its jurisdiction and is thus susceptible to security threats. 72 Sovereignty anxiety has led to some deplorable decisions by the government. For example, in the 1950s, the federal government forcefully relocated Inuit families from Québec to the High Arctic Archipelago to strengthen evidence of occupation and authority over the region. 73 However, boundary disputes between Canada and the US over the NWP have been relatively insignificant in the context of overall relations between the neighbours. As Canada places high importance on interoperability with US military forces and both countries greatly value their bilateral trade relationship, disagreement over the Arctic passage has had little impact on the cooperative relationship between the two North American nations or the stability of the Arctic Council.

Bilateral trade: East Asia and the United States

The NWP would serve as an alternate route to the Panama Canal, although the distance saved is relatively modest. Upon opening of the NWP, trade between the US and Northeast Asia would see the largest increase, particularly with China. The primary difference between a scenario in which only the NSR is used and a situation in which both Arctic shipping routes become fully operable is the significant increase in US exports to China. Compared to a negligible increase of less than one percent when only the NSR is available, the NWP would catalyse a thirteen percent increase in bilateral trade flows between the US and China.74 The European continent would be affected by an open NWP only in that trade diversion caused by the opening of the NSR would be reduced by usage of the NWP.75 Since this trade diversion was already very minor, European countries stand little to gain and little to lose from the opening of the NWP. Due to its remote location and hostile conditions, the NWP is less relevant to the future of Arctic shipping than the NSR. The general consensus, although admittedly lacking data, is that the NWP will never be competitive with the NSR or existing conventional trading routes.

China: an Arctic actor?

In terms of trade, the Chinese economy stands the most to gain from full operation of the NWP and the NSR. The Chinese economy is highly dependent on international shipping – foreign trade accounts for 46% of its GDP. Analysts predict that China could save between $60-120 billion annually by diverting trade through the NSR, thus the Chinese incentive to develop Arctic shipping routes is, to understate it, understandable.76 China has repeatedly advocated for unobstructed access to the NSR and NWP for all states, often employing the language of UNCLOS to assert that the Arctic is the “common heritage of all humankind”. UNCLOS maintains that foreign vessels are granted the right of “innocent passage” through territorial waters and free navigation through exclusive economic zones, all the while states retain full sovereignty over internal waters.77

Source: International Journal of Trade and Global Markets

The greatest obstacle to Chinese objectives is its lack of authority in the Arctic field. Although China is undeniably and rapidly gaining political and economic currency on a global scale, its lack of Arctic territory delegitimizes its desires in the face of demands and concerns put forward by the Arctic Eight: Canada, Russia, the United States, Denmark, Sweden, Finland, and Norway. As the possibility of open Arctic routes becomes a frequented topic of discussion in political and economic spheres, Chinese officials and affiliates have sought various means of establishing a position of power and legitimizing their claims to Arctic affairs. It seems to have been an uphill battle for the Chinese – China was denied observer status on the Arctic Council three times until its application was finally accepted in 2013. Still, this grants the Asian nation little authority in Arctic matters.

China has taken several steps to circumvent this disadvantage – what China lacks in political authority it has replaced with scientific and resource diplomacy. China has maintained a well-funded and expansive research apparatus in the Arctic region since the 1990s. An initiative known as the Ice Silk Road – a division of China’s One Belt, One Road global development strategy – is responsible for research and exploration regarding the role of northern sea lanes and railways in the expansion of China’s trade links. Furthermore, China established a permanent base, the Polar Research Institute of China, in Norway’s Svalbard archipelago in 2004.78 Through joint climate change and ecological studies, China continues to develop relationships with the Arctic Eight, and regularly participates in international forums such as Arctic Science Summit Week and the International Polar Year Programme.79

Perhaps most notably, China has pursued both wealth acquisition and bilateral relationships with circumpolar states by dramatically increasing its financial stake in Arctic matters over the last decade. Just between 2011 and 2013, Chinese state owned companies invested more than $16 billion in Canadian energy and accounted for half of total demand for Canadian minerals.80 Notably, Canada was chairing the Arctic Council at this time – one might reasonably surmise that China aimed to curry favour with the Arctic nation by becoming the largest trading partner and foreign investor in its Arctic region. China’s Arctic investments extend beyond North America – the Silk Road Fund and the China National Petroleum Corporation (CNPC) have significant stakes in Yamal LNG project in Russia.81

Although the Arctic Eight retain primacy, China is indubitably emerging as a key stakeholder in the Arctic field. Although China’s involvement in the Arctic has been met with some resistance in the past, it is not so contentious to claim that, as a major source of foreign investment, Chinese ambitions are becoming material to Arctic affairs. The Arctic is becoming an increasingly relevant component of China’s expansionist efforts in both hard and soft terms, and has been particularly important in bolstering economic and political relationships with Russia and Canada in the 21st century.

Summary

As Arctic ice melts, the potential for navigable trading routes along the NSR and the NWP increases. Commercial operation of the NSR would increase bilateral trade between northwest Europe and northeast Asia, with trade diversion negatively – but minutely – affecting smaller European countries. Gains from the North American equivalent are much less striking, as increased accessibility in the NWP will primarily serve tourism and pleasure craft rather than international trade. China stands the most to gain from joint operation of both Arctic routes. In the last decade, the Northeast Asian country has undertaken significant research and investment efforts to garner authority with Arctic nations and legitimize its position as an Arctic actor.

Still, there are many barriers and complications to Arctic shipping. Physical climatic conditions, lack of infrastructure, and Russian monopolies make for a very expensive Arctic pursuit. The mainstream media frequently overstates the potential for lucrative international shipping and understates the obstacles that stand in its way. This is not to say that shipping in the Arctic is necessarily impossible – merely that the picture is quite complicated and several hurdles must be overcome in order for the NSR and the NWP to become competitive with traditional international trading routes.

Part III: Oil & Gas

Russia

Russia’s Arctic strategy in the 21st century

According to the Russian Ministry of Natural Resources and Environment, the Russian Arctic shelf holds the equivalent of 80 billion tonnes of oil, eighty percent of which is located in the Barents and Kara seas. With decreasing sea ice coverage, offshore resources are becoming more accessible. Some estimate that retreating sea ice coverage will reveal up to two trillion cubic feet of natural gas and 100 billion barrels of oil.82 This, and diminishing resources in West Siberia, has brought offshore development into the spotlight of Russian Arctic policy.83 In light of increasingly accessible offshore resources, President Vladimir Putin and other Russian officials have stated their intention to transform the Russian Arctic into a “resource base of the 21st century”.84

Source: Carnegie Endowment for International Peace

The first comprehensive Russian Arctic strategy was adopted in 2009. It emphasized the importance of its Arctic waters – the Barents, Pechora, and Kara seas, and the Yamal peninsula – and the “Transport strategy of the Russian Federation for the period until 2030” stressed the development of the NSR as a means of improving the socioeconomic development of Northern Russia. In 2013, the same objectives were detailed when Russia adopted the “Russian Strategy of the Development of the Arctic Zone and the Provision of National Security until 2020”. These are two among several government decisions that reflect Russia’s heated interest in improving geological prospecting on its continental shelf, implementing large-scale resource projects, and developing transport infrastructure.85

Russia has often sought and reasserted territorial claims to Arctic waters under UNCLOS; repeatedly stating its view that the Arctic is “home” to Russia and other Arctic nations, and that it is the responsibility of the Arctic Council to define the “rules of the game” by which any nations seeking to develop the Arctic must abide.86 Domestically, the Russian government has enacted legislation to place a small handful of state-owned companies in a position to monopolize the exploitation of natural resources in Russia’s Arctic. Alongside Russia’s first comprehensive Arctic strategy, 2008 saw amendments to Russia’s Law on Subsoil Resources that limited access to shelf deposits to companies with over fifty percent state ownership and not less than five years worth of experience in marine exploration.87 This effectively restricted eligibility to just two entities: Gazprom and Rosneft, both major state-owned companies. While foreign companies still could, in effect, participate in the development of the Arctic shelf, this legislation forced them to do so in partnership with either Gazprom or Rosneft.

This has been met with resistance from some liberal-leaning state officials. The Deputy Prime Minister and the Minister of Natural Resources and Environment have repeatedly argued that such a concentration of licenses in state-owned companies stalls the development of Arctic. The Ministry of Natural Resources and Environment attempted to delay the granting of new licences and promoted a development program that would expand eligibility. When high ranking officials at Gazprom and Rosneft appealed to Putin, the President demanded that the licences in question be granted without further delay. By 2013, the licences granted to state-owned companies accounted for eighty percent of the Russian Arctic shelf.88 Despite the privileges granted to state-owned companies, Gazprom and Rosneft still lacked the necessary offshore experience and capital to develop the Russian Arctic shelf single-handed, and have been largely unable to deliver at expected levels.

Russia and the West

Despite the free-reign granted by Putin, natural resource development projects face significant obstacles. First, resource extraction on the Russian shelf and other Arctic zones will always be a specialized and costly affair due to the Arctic climate. The lack of infrastructure, geographic location, and volatile climate increase both real and opportunity costs of offshore exploration in the region. Coupled with fluctuating oil prices, international interests in offshore development have tempered in the last decade.89

Historically, western nations have been the largest market for and primary investors in Russia’s natural resource industry. These relationships are undergoing significant and complex changes. Following the onset of the conflict in Ukraine in 2014, Russia’s relationships with western nations generally suffered. Where the West and the Arctic overlap, Russian economic and political cooperation with Arctic actors seriously deteriorated. Although Russia’s publicly stated commitment to cooperation in the Arctic remains unchanged and Arctic cooperation has mostly continued normally, the economic sanction warfare that took place following the annexation of Crimea has hindered Russian offshore development. In particular, sanctions that prohibit western companies from providing certain goods, services, and technologies to Russia have forced Exxon and Rosneft to shelve a joint venture in offshore oil development.90

Turning east: Russian cooperation with China

With many bilateral relations suspended and festering mistrust between Russia and other circumpolar nations, the landscape for investment in Russian offshore exploration has shifted drastically. Without its western investors, Russia has to secure other sources of investment in order to undertake the costly and specialized matter of offshore resource development. The need for investment should not be understated. The Russian Ministry of Natural Resources and Environment estimates that geological prospecting on the Russian Arctic shelf will require $607 million by 2030, and that total development costs will amount to $500 billion by 2050 – no small sum.91

Even prior to the conflict in Ukraine, Russian documents reflected a desire to diversify its sources of investment and build economic relationships with the growing Chinese economy. The 2009 “Energy Strategy of Russia for the period up to 2030” stated a desire to redirect investment focuses to the East, and a 2012 article used in Putin’s election campaign claimed that Chinese development represented a “chance to catch the Chinese wind in the sails of [the Russian] economy”.92 Initially, the idea of cooperation in the oil and gas sector was limited to political declarations. However, following deteriorating relationships with the west in 2014 and reinforced by China’s mission to be taken seriously as an Arctic actor, the development of the partnership began to accelerate. In short, Russia’s emerging partnership with China has been driven by two primary factors. First, that the Ukraine crisis has caused political tensions between Russia and the West, and Russia holds a political intention to prove itself unreliant on western nations. Second, key actors in Russia’s oil and gas sector are lacking what China is looking to provide: investment and a diversified energy market.

Source: Federal Custom Service of the Russian Federation, from The Oxford Institute for Energy Studies

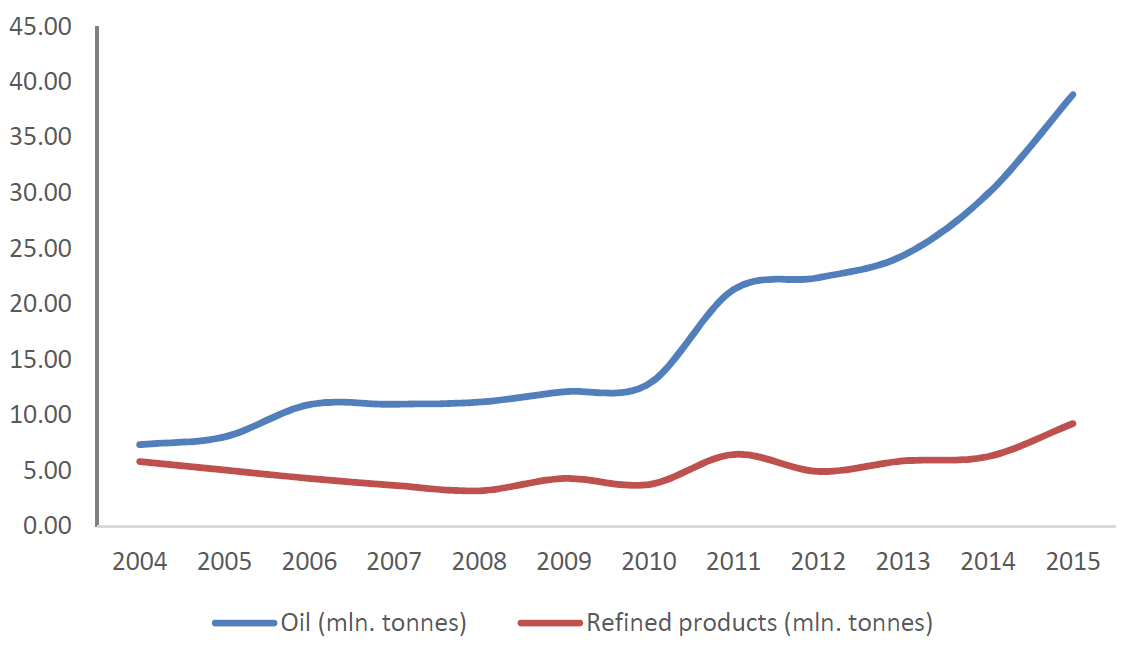

China has certainly obliged to the Russian desire to turn eastward. In 2009 alone, CNPC provided loans totalling $25 billion to Russian oil companies, essentially providing for the construction of the Eastern Siberia-Pacific Ocean oil pipeline that transports oil within Russia and to Daqing, China. Rosneft repaid China with 300 million tonnes of oil. In 2013, an agreement between Rosneft and the Chinese company Sinopec outlined the export of 10 million tonnes of oil per year for ten years in exchange for $85 billion. Rosneft and CNPC established two joint ventures – Vostok Energy Ltd and another in East Siberia – to develop hydrocarbons. In 2014, a historic gas deal was signed with China after a decade of negotiations that promised the delivery of 38 billion cubic metres per year.93

Source: Federal Custom Service of the Russian Federation, from The Oxford Institute for Energy Studies

Source: Federal Custom Service of the Russian Federation, from The Oxford Institute for Energy Studies

Despite China’s commitment to developing the Russian Arctic, the Russian government remains fearful of China becoming too influential in some parts of Russia and wary of Chinese expansion. Alongside its growing relationship, the Russian government has imposed measures to curb China’s authority in Arctic offshore exploration and deter its entrance into key sectors of the Russian economy. For example, when Rosneft listed shares for sale in 2006, China was only allocated the equivalent of $500 million – a meagre share compared to the $3 billion it was prepared to invest.94 So Russia’s intentions are reflected in its relations with China: non-Arctic states are welcome to invest, research, and participate in Arctic affairs, but only at the discretion of and under the limits set forth by Arctic nations. Furthermore, Russia’s cooperation with China in the oil and gas industry is illustrative of its entire Arctic strategy and the conflict between its political desire to enhance its sovereignty and its economic need to cooperate with other nations.

Diversifying the Chinese energy market: the Malacca Dilemma

As discussed, China has financed Arctic resource development as a means of justifying its involvement in Arctic matters. But the Chinese motive for nurturing a bilateral relationship with Russia and contributing to offshore development is twofold, owing to what has come to be known as the Malacca Dilemma. This refers to a Chinese strategic weakness: 78% of Chinese hydrocarbon imports pass through the Strait of Malacca, an incredibly narrow waterway controlled by Indonesia, Malaysia, and Singapore.95

Vulnerable to hostile shutdowns and potentially volatile political environments, China seeks to diversify its energy sources. Shipping hydrocarbons through Arctic waters and developing Russian offshore resources could alleviate some of China’s energy insecurity by redirecting imports.

Source: BP Statistical Review of Energy 2015, from The Oxford Institute for Energy Studies

Other Arctic Nations & Fossil Fuels

Norway

Among Arctic nations, Russia’s Arctic strategy provides the clearest and most consistent narrative: increase Chinese investments, expand offshore exploration, and consolidate the Russian Arctic into a resource base. Other Arctic nations’ approaches to Arctic hydrocarbon resources are not so straightforward. Norway, for example, faces tensions between growing concerns for climate change, maintaining national productivity, and pressure from its Russian neighbour.

In April 2019, Norway’s Labour Party withdrew exploration and drilling off the Arctic Lofoten islands, which came as a disappointment to many industry leaders.96 A month prior to this controversial ruling, Norway’s sovereign fund announced it would no longer invest in 134 companies that explore for oil and gas, but would retain stakes in large firms such as BP and Shell that have renewable energy divisions. This announcement comes alongside the green light given by the Norwegian government for the $1 trillion oil fund – the world’s largest sovereign wealth fund – to invest in renewable energy projects not listed on the stock market, in an effort to redirect wealth accumulated through fossil fuels to more sustainable energy sources.97 This illustrates concerns for the long-term of the Norwegian economy and climate, and growing doubts about the sustainability – both environmental and economic – of the oil and gas industry as calls for climate action echo throughout the country and renewable alternatives become progressively more attractive.

The Norwegian energy landscape is far from green, however. With oil and gas accounting for over half of total national exports, government efforts to pull back from hydrocarbon development are met with significant resistance from the domestic industry. Norway’s largest producer, the state-controlled Equinor ASA, and the Norwegian Oil and Gas Association are among those who have expressed hostility and concerns regarding the stability of the industry in light of the Labour Party’s recent ruling against drilling off the Lofoten islands. The nation’s largest oil union and long time ally of the Labour Party, Industry Energy, attacked the new stance on drilling. Its leader is quoted: “It creates imbalances in the policy discussions for an industry that’s dependent on a long-term perspective and we can’t accept that.”98

Although one might refute Industry Energy’s claim and argue that the long-term simply doesn’t exist for an industry that is by definition finite and nonrenewable, the Norwegian government has supported expansion of drilling in areas other than the Arctic Lofoten islands while the Ministry of Petroleum and Energy has announced plans to expand drilling in the Barents Sea. The Ministry might escape some heavy criticism by climate activists and civilians in restricting the new licenses to “predefined areas” – those which have already been opened for exploration and are equipped with existing infrastructure.99 Still, the oil and gas industry is hardly revolutionized.

While current exploration has been largely restricted to the southern parts of the Barents Sea, Russian exploration along the maritime border has inspired a resurgence in Norway’s interest in the sea’s Arctic resources. The head of the Norwegian Petroleum Directorate (NPD) has said Norway will prepare to claim its share of oil and gas if Russian exploration along the Barents boundary is fruitful. The NPD has pledged to conduct seismic surveys of geological structures that straddle the Russian border, with its leader Bente Nyland asserting what are essentially efforts to keep up with the Joneses: “Let’s say [the Russians] started to drill close to [the border] and there is a cross-border structure, then, of course, Norway would like to get the resources that belong to Norway.”100

Norway has embraced what some call a “measured view” of melting Arctic sea ice and the ensuing access to resources by implementing carbon taxes and funding emissions-limiting technologies while still actively developing Arctic hydrocarbons and upholding its oil production legacy.101 At least more so than its Russian neighbour, Norway is moving towards a more sustainable energy market. With an undeniably low bar set by the Russians, however, there remains little cause for celebration. Sustainably-minded policy concessions, such as divestment from coal, tiptoe around the great beast of the Norwegian oil industry. Investments in green technologies and divestments from coal function as somewhat of a distraction, while business as usual in the oil industry continues behind the scenes. As Europe’s largest exporter of crude oil, Norway has a long way to go before justifiably calling itself a green economy.

Source: Daniel Workman, World’s Top Exports

Canada

Quite like Norway, the Canadian government is faced with reconciling the burgeoning threat of climate change with its economic dependence on fossil fuel exports. As the sixth largest energy producer, fourth largest exporter, and eighth largest consumer, the Arctic giant is hardly a trailblazer in sustainable energy.102 Again, not dissimilar to Norway, Canadian oil and gas policies make for a mixed bag. Most recently, just one day after declaring a national climate emergency, Prime Minister Justin Trudeau approved a pipeline expansion to triple the amount of crude oil that moves from the Alberta tar sands to the Pacific Coast for international shipment. The Liberal government has vowed to invest every dollar earned from the $5.5 billion expansion in projects to facilitate Canada’s transition to clean energy.103

With regards to the Arctic in particular, the government stance less ambiguous. In 2016, the Canadian government instituted a five year moratorium on offshore drilling in Canada’s Arctic. Canada faces many of the same financial and logistical complications to offshore drilling as Russia – high real and opportunity costs, uncertainty, hostile weather conditions, and a gaping need for international investment. With abundant resources in much less expensive and much less risky areas on the west coast, growing domestic and international pressure to adopt more aggressive measures to combat climate change, and fickle oil prices on the global market, Arctic offshore drilling is understood as a high-risk low-reward endeavour.104 Even prior to the federal moratorium, oil and gas activity in the Arctic had been on a declining slope for several years. Industry giants BP and Imperial Oil Ltd have indefinitely suspended development in the Beaufort Sea, constituent of the Canadian Arctic. For reference, there have been over one hundred wells drilled in the Beaufort Sea since the 1970s, but only one drilled in the last twenty years.105 Imperial Oil Ltd and Royal Dutch Shell have also dissolved partnerships that would facilitate the transport of oil through Canada’s Arctic territories. The course towards a complete standstill of Arctic hydrocarbon development in Canada has been seemingly unbothered by melting ice and newfangled offshore accessibility, as the Liberal government stands by the federal moratorium on Arctic drilling and advocates for environmentally responsible resource development that allows for both scientific and Indigenous input.106

The unforgiving Canadian policy on Arctic development is an outlier among Arctic nations, particularly with Russia and Norway ploughing full steam ahead. Like any stringent policy, the federal moratorium has faced significant criticism from its northern territories whose economies are largely dependent on the Arctic oil and gas industry. Provincial GDP in the Northwest Territories has shrunk by $1 billion in resource development, prompting northern political leaders to urge the federal government to follow suit with Russia and Norway, despite concerns about climate change.107 As institutional investors grow ever more hesitant to fund projects in Canada’s north due to a lack of long term perspective on energy development – whether it be renewable or nonrenewable – northern leaders criticize the moratorium for merely providing something of a red herring in terms of climate action for a government that still relies heavily on the fossil fuel industry, all the while damaging the livelihoods of Indigenous peoples and Arctic inhabitants.108

While Canada has taken a more aggressive and inflexible stance on Arctic resource development than some of its European counterparts, transitioning to a green energy economy is no small feat for the Arctic nation – the Canadian fossil fuel industry has not yet waved the white flag of surrender. If Norway and Russia continue to expand Arctic production and Canada’s market becomes increasingly less competitive, the logic of the moratorium – subject to review in 2021 under a potentially new government – may come under question. Like Norway, the Canadian government’s fundamental challenge is balancing evermore urgent environmental considerations with its economic dependence on fossil fuel extraction.

USA

At the Arctic Oil & Gas Symposium in Calgary in 2016, former President Barack Obama enacted the same moratorium as Canadian Trudeau to restrict offshore drilling in the Arctic.109 More recently, President Trump has attempted to repeal the moratorium and resume drilling in the Alaskan Arctic. An Alaskan federal judge ruled that revoking such a ban was beyond presidential authority, and Trump’s rescinding of the ban was actually illegal.110 Despite this legal obstacle, it would be generally unsurprising if Trump was able to circumvent technicalities and resume Arctic drilling, rolling back on yet another Obama-era climate policy. In addition to Canada’s ban on Arctic drilling, Trudeau has expressed a desire to reduce Canada’s reliance on the US as a fossil fuel customer and increase shipments to new buyers in Asia.111 It is unclear whether potential rollbacks by its largest trading partner would inspire the US government to hesitate on annulments such as the joint Arctic offshore moratorium or motivate it to increase its Arctic offshore presence, become competitive with Canadian exports, and diversify its energy market. Based on Trump’s notorious climate change denial and support for extractive industries, something along the lines of the latter seems a more likely scenario.

With legal obstacles to overcome, the future of American Arctic offshore exploration is unclear. Given the administration’s general lack of concern for climate change issues and potential anxiety caused by Russia’s offshore expansion, further development of American Arctic hydrocarbons would be hardly surprising – legal hurdles may provide, at best, a period of stagnancy.

Summary

Russia’s offshore hydrocarbon resources present a potentially lucrative endeavour. However, state-owned companies – the only entities with authorization to explore and extract – struggle in the face of high costs and harsh climates. Whereas Russia once turned westward for assistance in mastering these challenges, the annexation of Crimea in 2014 has changed Russia’s international reputation and galvanized a solidification of relations with China. China’s massive investments in Russian offshore oil and gas have served to satisfy the industry’s financial demands, meanwhile buttressing China’s venture to become a source of authority in Arctic affairs and diversify its energy imports.

Other Arctic nations, such as Norway, Canada, and the US, present a more nuanced yet indeterminate approach to Arctic offshore development. The relationships between climate change and economic loss are increasingly disseminated, understood, and accepted by the mainstream. Failing a transition to low-carbon technologies, some estimates place the total potential loss at $1.3 trillion, with the US and Canada most exposed at $545 billion and $110 billion respectively.112 Countries such as Norway and Canada, whose economies are sustained by the fossil fuel industry, are beset with a complicated picture. Amid snowballing domestic and international calls for climate action, the economically-handicapped Norwegian and Canadian governments must find the appropriate intersection between financial and environmental considerations. Both Arctic nations are proceeding with many fossil fuel projects, but have pledged significant investments to renewable energies and technologies. Under a more radical government, the United States propounds equivocal messages regarding the future of American Arctic offshore exploration. Although the current government has been clear in its intention to disregard climate warnings and resume offshore exploration, rollbacks on sustainably-minded policies are hindered by legal obstacles for the time being. Questions remain as to the influence of neighbour on neighbour – will Norway be cajoled by Russian offshore development, and Canada by the US?

Discussions of offshore development often prompt questions of the potential for conflict in the Arctic. Actually, there is little basis for a causal relationship between offshore oil and gas in the Arctic and international conflict. There exists a common misperception that offshore resources remain unclaimed and unaccounted for by established boundary lines. In fact, approximately 90% of circumpolar oil and gas is located in the Exclusive Economic Zones or territories of the Arctic states themselves, and thus falls under the jurisdiction of littoral states.113 The remaining ten percent is guarded by extremely hostile weather conditions and high real and opportunity costs, thus there is little incentive to engage in conflict over territorial claims to natural resources. This alone should suffice as a rebuttal to claims of a brewing conflict – there is no wealth of unclaimed Arctic riches to be fought over. Thus the answer to questions and qualms regarding a potential outbreak of dispute over oil and gas resources is quite simple: it is highly unlikely.

If conflict occurs in the Arctic, it is much more likely to materialize as spill-over from disputes unrelated to the region itself. Arctic security cannot be entirely divorced from broader security considerations, and should be considered a constituent matter under the umbrella of national security. One must remember “the Arctic” refers to a climatic rather than political territory, acknowledging its fragmentation in that each Arctic territory is susceptible to the individual political decisions and relationships of its national government. By way of speculative examples, international tensions with Russia following the annexation of Crimea or strained relations with a politically radical United States are more likely to become the foundations of conflict than strictly regionally-based clashes over resource ownership. Although this is the more likely scenario, it is still quite unlikely, and even less likely to occur in parallel with melting Arctic ice. The Arctic Council has actively and repeatedly stressed its commitment to cooperative and peaceful relations among Arctic states, both as individual Arctic nations and as a unified organization.114 Arctic nations have historically been unified by the Arctic Council’s philosophies on cooperation, and have a demonstrated history of fidelity to peaceful resolution efforts. The lack of incentive for conflict this history of cooperation make for a very low likelihood of Arctic conflicts and threats to security.

Conclusion

The Arctic is warming at twice the rate of the global average. The 21st century hosts record high temperatures and record low ice coverage – the twelve lowest minimum sea ice extents in the satellite record have occurred in the last twelve years. Although some of the decline in sea ice can be explained by seasonal fluctuation and oscillation patterns inherent to the Arctic climate system, current statistics are both beyond the observed limits of the natural Arctic climate and consistent with anthropogenic climate change. Declining sea ice is worrisome not only for the Arctic climate itself, but for the stability and regulation of global climate systems. With its relatively high albedo, the Arctic functions as a thermostat for the rest of the planet – to disrupt Arctic climate systems is to sacrifice the stability of the global climate.

Climate models predict a completely ice-free Arctic summer is likely to occur within the 21st century. Although estimates differ as to exact dates, the general consensus places an ice-free summer towards the end of the century. Retreating ice reveals political, economic, and environmental opportunities and concerns. Among the most popular subjects of discussion inspired by melting sea ice is the future of trade, and the possibility of newly-available shipping routes composed by Arctic waters. The Northern Sea Route, which passes through Russian jurisdiction and connects northeast Asia with northwest Europe, has been a particularly fashionable topic. In comparison to the conventionally-used Suez Canal, the NSR would reduce travel distances by almost half. This would increase bilateral trade flows between Japan, South Korea, and China with major western European centres, resulting in minor trade diversion from smaller European countries. However, gains from trade through the NSR are contingent on a multitude of factors that remain largely unresolved. Unpredictable and hostile weather conditions, the Russian monopoly on transit fees, steep insurance premia, and an exigent lack of infrastructure are among the primary hurdles to financially-sensible use of the NSR. Notwithstanding the settlement of these obstacles, use of the NSR simply will not be lucrative.

The Northwest Passage is another trading route that may become available for use as sea ice coverage declines. Passing through the Canadian Archipelago, the NWP would serve as an alternative to the Panama Canal. Compared to the NSR, the potential distance savings from the NWP are far less striking, thus making it a less attractive shipping route. Coupled with a cavernous lack of data and harsh weather conditions, the NWP provides more potential for tourism than it does for trade. Operation of the NWP, although increasing, remains minimal and restricted almost exclusively to pleasure craft and government vessels. Despite modest reductions in transit time, the NWP does not present a practical substitute for the Panama Canal.

The popular ear lends next to the question of offshore oil and gas in increasingly accessible Arctic territories. Arctic nations are faced with reconciling the exponentially-growing threat of climate change with a colossal economic dependence on the fossil fuel industry. Today, Russia is unfolding plans to expand offshore drilling, turning to an eager China for investment as relations with the West decay. Although bridled by legal obstacles, the US has indicated its desire to follow Russian suit and increase offshore drilling in the Arctic. Both Canada and Norway seem to be attempting to curate an image of sustainability with Canada’s moratorium on Arctic offshore drilling and both nations’ investments in environmentally-friendly technologies. However, a truly sustainable energy market remains more talk than walk – the Canadian and Norwegian oil and gas industries proceed unchecked.

Many mainstream media publications immensely misrepresent the current geopolitical state of affairs in the Arctic. Claims of an “Arctic Scramble”, a “new Cold War”, and a “race to the North” dominate many headlines and conjure images of Arctic nations frothing at the mouth, neighbour against neighbour in a heated competition for Arctic hydrocarbon resources.115 Such publications also exaggerate the promise of the NSR as an international trading route, again proposing an image of tensing relations between Arctic states over access to and control over Arctic waters.

These headlines sell – but they are ill-founded. Such renderings overlook the complexities and nuances of the Arctic situation: the hostile Arctic climate, the logistical and financial barriers to Arctic shipping, and the increasingly unconvincing logic of offshore expansion. Furthermore, these ominous allegations neglect to acknowledge the philosophy of cooperation set forth by the Arctic Council and respected by Arctic nations. The design of the Arctic Council promotes robust partnerships in its requirement of consensus, which effectively functions as veto power, and the explicit exclusion of military affairs from its agenda. This, coupled with the separation that exists between government departments on a domestic level, has allowed Arctic nations to compartmentalize issues and separate international and regional arenas from one another, and remain aligned with the Arctic Council’s policy and history of cooperation. The development of the Arctic region relies on the management of interdependence, and thus supersedes questions of sovereignty.116